Understanding compound interest is essential for anyone looking to make informed financial decisions. Whether you’re taking out a loan, investing, or saving, knowing how to calculate compound interest can help you understand your financial situation. This comprehensive guide will help you grasp the compound interest formula, its applications, and how real-life loan examples can illustrate its impact.

What is Compound Interest?

Compound interest formula refers to the interest that is calculated on the initial principal amount and also on the accumulated interest from previous periods. The formula for compound interest allows you to determine how much interest will accumulate on your principal over time, effectively compounding the interest through regular intervals.

The Formula

The compound interest can be calculated using the formula:

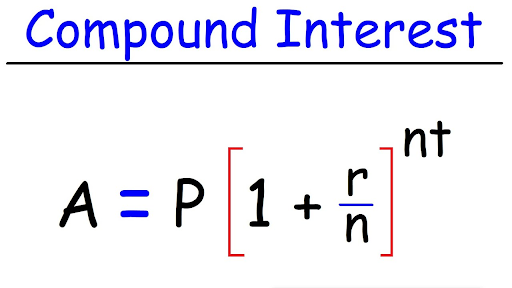

A=P(1+rn)ntA = P left(1 + frac{r}{n}right)^{nt}A=P(1+nr)nt

Where:

A = the future value of the investment/loan, including interest

P = the principal investment amount (the initial deposit or loan amount)

r = the annual interest rate (in decimal)

n = the number of times that interest is compounded per year

t = the number of years the money is invested or borrowed

By breaking down this formula, you can see how each variable impacts the overall amount.

How to Calculate Compound Interest

Let’s walk through a step-by-step process on how to use the compound interest formula effectively.

Identify Variables

Determine your principal amount (P), the annual interest rate (r), how often the interest compounds (n), and the total number of years (t).

Convert Interest Rate

Ensure that the annual interest rate is in decimal form. For example, if your interest rate is 5%, you will use 0.05 in the formula.

Substitute

Insert the values into the formula.

Calculate

Perform the calculations in the correct order, applying the exponent and any multiplication or addition.

Example Calculation

Imagine you invest $1,000 at an annual interest rate of 5%, compounded quarterly (4 times a year), for 3 years.

P = 1000

r = 0.05

n = 4

t = 3

Substituting into the formula:

A=1000(1+0.054)4×3A = 1000 left(1 + frac{0.05}{4}right)^{4 times 3}A=1000(1+40.05)4×3

Calculating:

A=1000(1+0.0125)12A = 1000 left(1 + 0.0125right)^{12}A=1000(1+0.0125)12

A=1000(1.0125)12A = 1000 left(1.0125right)^{12}A=1000(1.0125)12

A=1000×1.1616A = 1000 times 1.1616A=1000×1.1616

A≈1161.62A approx 1161.62A≈1161.62

So, after 3 years, your investment will grow to approximately $1,161.62.

Real-Life Loan Example: Home Loans

When you’re considering home loans, the impact of compound interest can be substantial over time. Let’s explore how this works through a real-life example.

Case Study: Home Loan Calculation

Suppose you take out a home loan of $250,000 at a 4% annual interest rate, compounded annually, for 30 years.

P = 250,000

r = 0.04

n = 1 (compounded annually)

t = 30

Using the formula, we can calculate the total amount to be paid at the end of the loan period.

A=250000(1+0.041)1×30A = 250000 left(1 + frac{0.04}{1}right)^{1 times 30}A=250000(1+10.04)1×30

A=250000(1.04)30A = 250000 left(1.04right)^{30}A=250000(1.04)30

A=250000×3.2434A = 250000 times 3.2434A=250000×3.2434

A≈810,850A approx 810,850A≈810,850

This means that over 30 years, you would pay approximately $810,850 in total, including $560,850 as interest.

Pre-EMI and Its Impact

Before your house construction is completed, you may have to pay a pre-EMI (Equated Monthly Installment). This is a process in home loans where borrowers pay only the interest on the availed loan during the construction period. This concept is also useful to understand when managing smaller borrowings like a Personal Loan 60k, where interest-only payments may apply in certain scenarios.

Pre-EMI Calculation Example

Consider a home loan of $250,000 at a 4% interest rate, compounded monthly, where the construction will take 2 years.

Monthly interest rate = 0.0412frac{0.04}{12}120.04 = 0.00333

Pre-EMI per month = Principal × Monthly Interest Rate

Pre-EMI = 250,000×0.00333=833.33250,000 times 0.00333 = 833.33250,000×0.00333=833.33

For 24 months, you would then pay 833.33×24≈20,000833.33 times 24 approx 20,000833.33×24≈20,000 purely in interest.

While the loan amount remains the same, paying pre-EMI can help you better manage your finances during the construction period.

Registration Fees for Loans

While understanding the compound interest formula is vital for calculating your loan payments, other costs arise when taking out loans. Registration fees are often a fixed percentage of the loan amount. Knowing the registration costs involved can help you budget effectively.

Registration Fee Example

In many cases, registration fees may range from 1-2% of the loan amount:

For a $250,000 loan with a 1.5% registration fee, the cost would be 250,000×0.015=3,750250,000 times 0.015 = 3,750250,000×0.015=3,750.

Creating a comprehensive financial plan must incorporate all these costs, ensuring no unexpected expenses derail your budget.

Conclusion

Understanding the compound interest formula is critical in effectively managing loans, investments, and savings. By mastering this formula and applying real-life examples such as home loans and pre-EMI payments, you’ll be better equipped to navigate your financial future. This knowledge not only empowers you to make informed decisions but can also lead to significant savings over time. Remember, always account for additional costs such as registration fees and other potential charges to avoid surprises in your financial planning. With diligence and understanding, you can turn the complexities of compound interest into a tool for financial success.